Balance Sheet Basics for Small Business Owners | Simple Guide

Learn what a balance sheet is, why it matters, and how to read one. Simple guide for small business owners with no accounting background. Real examples included.

REPORTINGBALANCE SHEET

Jerry Blanco

10/9/20255 min read

Your Business's Financial Story in One Simple Report—And Why It Matters More Than You Think

You know that feeling when you're trying to figure out if your business is actually doing well, but you're not quite sure where to look? You're making sales, paying bills, and somehow there's money in the bank—but is that enough? Are you building something solid, or just spinning your wheels?

This is where your balance sheet comes in. And I promise, it's not as scary as it sounds.

Think of your balance sheet as a financial snapshot of your business—like pausing a video to see exactly where you stand at one specific moment. While your income statement (also called a profit and loss statement) shows you how you made or lost money over time, your balance sheet shows you what you have right now.

Let's break this down in a way that actually makes sense.

What Exactly Is a Balance Sheet?

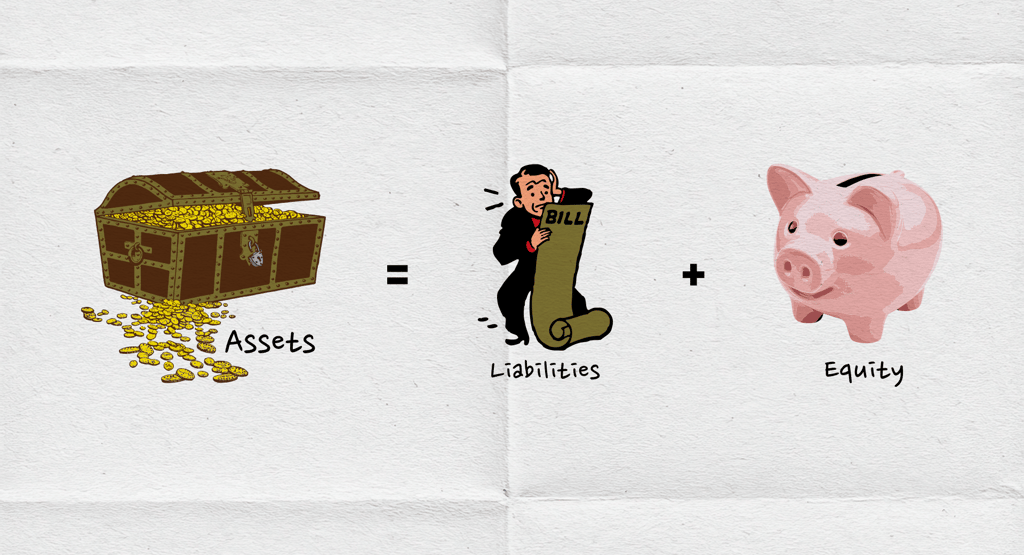

Your balance sheet is divided into three main sections, and here's the beautiful part: they always balance out (hence the name). The formula is simple:

Assets = Liabilities + Equity

Don't let these terms intimidate you. Let me translate:

Assets = What you own

Liabilities = What you owe

Equity = What's actually yours (your ownership stake in the business)

Think of it like buying a house. If you purchase a $300,000 home with a $240,000 mortgage, your asset is the house ($300,000), your liability is the mortgage ($240,000), and your equity is the $60,000 difference—that's the part you truly own.

Your business works exactly the same way.

Breaking Down Assets: What Your Business Owns

Assets are resources your business owns that have value. They're typically listed in order of liquidity—fancy term for "how quickly you can turn them into cash."

Current Assets (Can be converted to cash within a year)

Cash and Cash Equivalents: This is straightforward—money in your checking account, savings account, or that PayPal business account. If you have $5,000 sitting in your business checking, that's a current asset.

Accounts Receivable: Money customers owe you for work you've already done. If you invoiced a client $2,500 last week and they have 30 days to pay, that $2,500 is an asset—you earned it, even though you haven't received the cash yet.

Inventory: If you're a product-based business, this is the stuff sitting in your garage or warehouse waiting to be sold. For service businesses, you typically won't have this.

Fixed Assets (Long-term resources)

These are big-ticket items you'll use for more than a year:

That laptop you bought for $2,501

Your delivery van

Office furniture

Equipment and machinery

Here's something important: these assets depreciate (lose value) over time, which your balance sheet reflects. Your three-year-old laptop isn't worth $1,800 anymore, even though you paid that originally.

Understanding Liabilities: What You Owe

Liabilities are your business's financial obligations—money you need to pay back.

Current Liabilities (Due within a year)

Accounts Payable: Bills you haven't paid yet. If you received a $300 invoice from your web designer last week that's due in 15 days, that's accounts payable.

Credit Card Balances: Whatever you owe on business credit cards.

Short-Term Loans: Any portion of a loan due within the next 12 months.

Payroll Taxes Owed: Money you've collected from employee paychecks but haven't sent to the government yet (this one is critical—the IRS really cares about this).

Long-Term Liabilities (Due after one year)

Business loans or lines of credit

Equipment financing

Any other debt with payments extending beyond 12 months

Equity: The Part That's Actually Yours

This is the fun part—equity is what you actually own in your business after subtracting everything you owe from everything you have.

For sole proprietors and partnerships, this section is called "Owner's Equity." It includes:

Initial Investment: The money you put in when you started

Additional Contributions: Any personal money you've added since

Retained Earnings: Profits you've kept in the business instead of taking out

Owner's Draws: Money you've taken out for personal use (this reduces equity)

Here's a real example: Let's say you started your graphic design business by putting in $5,000. Over two years, you've made $80,000 in profit but took out $60,000 to live on. Your equity would be $25,000 ($5,000 + $80,000 - $60,000).

How the Balance Sheet Connects to Your Other Financial Statements

This is where it gets really useful. Your three main financial statements work together like chapters in a book:

Income Statement: Shows how you made money (or didn't) over a period—like last month or last year

Balance Sheet: Shows what you have and owe right now

Cash Flow Statement: Shows how cash moved in and out of your business

The connection? Your net income from the income statement flows directly into retained earnings on your balance sheet. And the cash on your balance sheet is explained by your cash flow statement.

Understanding this connection helps you see the complete picture. You might be profitable on paper (income statement shows positive net income) but still scrambling for cash (balance sheet shows low cash, high accounts receivable).

Why Your Balance Sheet Actually Matters

For Making Decisions: Should you buy that new equipment or finance it? Your balance sheet shows whether you have the cash assets available or if you'd be over-leveraging with more debt.

For Getting Financing: Banks and lenders require balance sheets before approving business loans. They want to see your debt-to-equity ratio—basically, are you already drowning in debt?

For Tracking Growth: Comparing balance sheets from December to December shows whether your business equity is actually growing or if you're just treading water.

For Tax Planning: Understanding your assets helps you maximize depreciation deductions. Knowing your liabilities helps you plan for deductible interest expenses.

Your Action Plan: Start With These Simple Steps

Step 1: If you're using accounting software like QuickBooks or Xero, you already have a balance sheet—you just need to run the report. Look for "Reports" in the menu, then find "Balance Sheet" under financial statements.

Step 2: If you're still using spreadsheets (no judgment!), start listing everything in three columns: Assets, Liabilities, and Equity. Make sure Assets = Liabilities + Equity. If they don't balance, you've missed something.

Step 3: Review your balance sheet monthly, not just annually. Set a recurring calendar reminder for the first week of each month to check last month's balance sheet.

Step 4: Calculate your current ratio (Current Assets ÷ Current Liabilities). If it's above 1, you have enough short-term assets to cover short-term debts. Below 1? Time to have a serious conversation about cash flow.

Step 5: Watch your debt-to-equity ratio (Total Liabilities ÷ Equity). If this number keeps climbing, you're financing growth with debt instead of profits—not always bad, but something to monitor.

The Bottom Line

Your balance sheet isn't just a report you create once a year for your accountant or the bank. It's a powerful tool that shows you the financial health of your business in black and white.

The entrepreneurs who understand their balance sheets make better decisions about hiring, purchasing, and expansion. They know when they can afford to invest and when they need to focus on collecting receivables or paying down debt.

You don't need to be an accounting expert to read your balance sheet—you just need to understand the basics. And now you do.

Ready to take control of your business finances? Your balance sheet is waiting to tell you a story. It's time to start listening.