Income Statement Guide for Small Business Owners

How This Simple Financial Report Reveals Whether Your Business Is Actually Making Money (And What to Do About It)

REPORTINGBOOKKEEPINGINCOME STATEMENT

Jerry Blanco

10/12/20256 min read

How This Simple Financial Report Reveals Whether Your Business Is Actually Making Money (And What to Do About It)

You're running your business, hustling every day, and your bank account feels healthy. But are you actually profitable? That's the million-dollar question—and your income statement holds the answer.

If you've ever stared at financial reports feeling completely lost, you're not alone. Most small business owners I work with started their ventures because they're passionate about what they do, not because they love numbers. But here's the thing: understanding your income statement isn't about becoming an accountant. It's about gaining clarity on whether your hard work is translating into real profit.

Think of your income statement as your business's report card. It tells the story of your financial performance over a specific period—whether that's a month, quarter, or year. And once you understand how to read it, you'll make smarter decisions about pricing, expenses, and growth.

Let me walk you through everything you need to know.

What Exactly Is an Income Statement?

An income statement (also called a profit and loss statement or P&L) is a financial report that shows your revenue, expenses, and profit over a specific time period. It answers one fundamental question: Did I make money or lose money during this period?

Unlike a snapshot of what you own (that's your balance sheet), the income statement is more like a movie—it shows the action that happened between two dates.

Here's the basic formula: Revenue - Expenses = Net Income (or Net Loss)

Simple, right? But the details matter, and that's where most business owners get tripped up.

The Three Financial Statements: What's the Difference?

Before we dive deeper into the income statement, let's clear up the confusion between the three main financial reports every business has:

Income Statement (Profit & Loss Statement) Shows your revenue, expenses, and profit over a period of time (like January through March). It tells you if you're making money.

Balance Sheet Shows what you own (assets), what you owe (liabilities), and what's left over (equity) at a specific point in time. Think of it as a financial snapshot on a particular date.

Cash Flow Statement Shows how cash moved in and out of your business during a period. You can be profitable on paper but still run out of cash—this statement shows you why.

For today, we're focusing on the income statement because it's the report most small business owners need to understand first. It's your financial scoreboard.

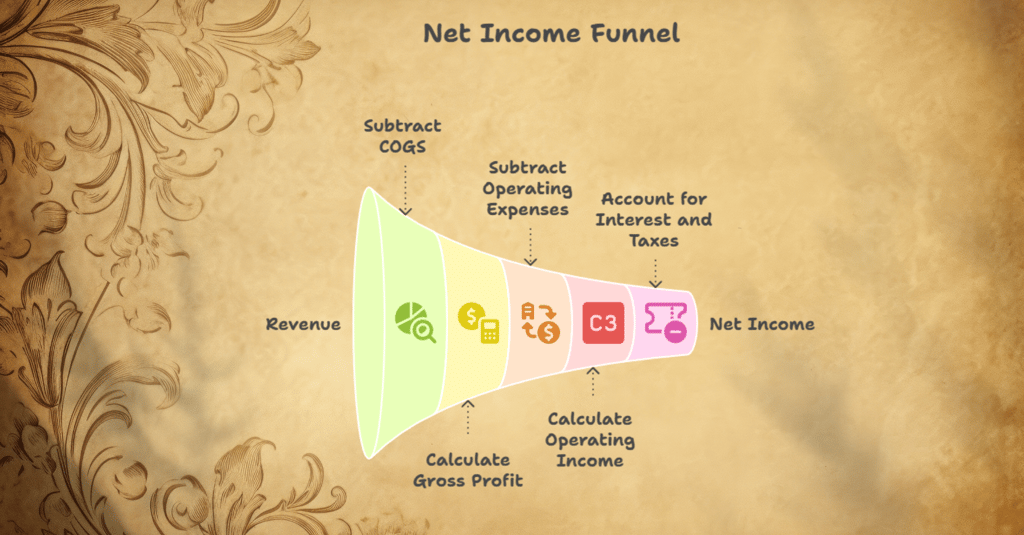

Breaking Down Your Income Statement: Line by Line

Let me walk you through what you'll actually see on an income statement, using plain English.

Revenue (or Sales)

This is all the money your business earned from selling products or services during the period. If you're a freelance graphic designer, this is your design fees. If you run a coffee shop, it's everything you sold.

Example: You invoice clients $15,000 in March. That's your revenue.

Key point: Revenue is recorded when you earn it, not necessarily when cash hits your bank. If you invoice a client in March but they pay in April, it still counts as March revenue.

Cost of Goods Sold (COGS)

These are the direct costs of producing whatever you sell. For product-based businesses, this includes materials and labor to make the product. For service businesses, this might be subcontractor fees or specific project costs.

Example: That coffee shop spent $4,000 on coffee beans, milk, and cups to make the drinks they sold.

Not every business has COGS. If you're a consultant selling your time and expertise, you probably don't have traditional cost of goods sold.

Gross Profit

This is what's left after subtracting your COGS from revenue: Revenue - COGS = Gross Profit

This number tells you how much money you have available to cover your operating expenses and (hopefully) make a profit.

Operating Expenses

These are all the costs of running your business that aren't directly tied to making your product or service. Common examples include:

Rent and utilities

Salaries and wages

Marketing and advertising

Insurance

Office supplies

Professional fees (like bookkeeping—hint, hint!)

Software subscriptions

Phone and internet

Example: Your monthly operating expenses total $7,500 for rent, utilities, marketing, your part-time assistant, and software.

Operating Income

Subtract your operating expenses from gross profit: Gross Profit - Operating Expenses = Operating Income

This shows you the profit from your core business operations before considering things like interest and taxes.

Other Income and Expenses

This section includes items outside your normal operations:

Interest income (from business savings accounts)

Interest expense (from business loans)

One-time gains or losses

Net Income (The Bottom Line)

After accounting for everything—all revenue, all expenses, interest, and taxes—you arrive at your net income. This is your actual profit (or loss).

If this number is positive: Congratulations! Your business made money during this period.

If this number is negative: Your business spent more than it earned. This isn't always bad (especially for growing startups), but you need to understand why and how long you can sustain it.

Sample Income Statement Format

Here's what a simple income statement might look like for a freelance marketing consultant:

ABC Marketing Services

Income Statement

For the Month Ended March 31, 2025

Revenue

Consulting Fees $15,000

-----------------------------------------

Total Revenue $15,000

Cost of Goods Sold

Subcontractor Fees $2,000

-----------------------------------------

Total COGS $2,000

Gross Profit $13,000

Operating Expenses

Home Office Rent $1,200

Software Subscriptions $450

Marketing & Advertising $800

Professional Development $200

Insurance $150

Phone & Internet $100

Office Supplies $75

Professional Fees $300

-----------------------------------------

Total Operating Expenses $3,275

Operating Income $9,725

Other Income/(Expenses)

Interest Income $15

-----------------------------------------

Total Other Income $15

Net Income $9,740

In this example, ABC Marketing Services brought in $15,000, spent $2,000 on subcontractors and $3,275 on operating expenses, and ended up with a profit of $9,740 for March. That's a healthy 65% profit margin!

Why You Should Review Your Income Statement Monthly

Most small business owners only look at their income statement when filing taxes—and that's a huge mistake. Here's why monthly reviews matter:

1. Catch Problems Early If expenses are creeping up or revenue is declining, you want to know now, not at year-end when it's too late to course-correct.

2. Make Informed Decisions Should you hire that assistant? Invest in new equipment? Raise your prices? Your income statement provides the data you need to decide confidently.

3. Understand Your Profit Margins Knowing your gross profit margin and net profit margin helps you price services correctly and identify which products or services are most profitable.

4. Track Trends Over Time Comparing your March income statement to February, or this March to last March, reveals patterns. Are summers slow? Is that new marketing campaign working?

5. Prepare for Tax Time Regular reviews mean no surprises when tax season arrives. You'll already know your profit picture and can plan accordingly.

Action Steps: What to Do Right Now

Here's how to start using your income statement effectively:

Step 1: If you're using accounting software (QuickBooks, Xero, FreshBooks, Wave), pull up your income statement for last month. Most software has this report under "Reports" or "Financials." Look for "Profit & Loss" or "Income Statement."

Step 2: Block 30 minutes on your calendar at the same time each month—I recommend the first week of the new month—to review your income statement. Make this a non-negotiable appointment with your business.

Step 3: Ask yourself these questions as you review:

Did revenue meet my expectations? If not, why?

Which expense categories were higher than expected?

What's my net profit margin? (Net Income ÷ Revenue × 100)

Is this sustainable? Can I afford my lifestyle on this profit?

Step 4: Compare this month to last month and to the same month last year. What changed?

Step 5: Based on what you discover, identify ONE action you can take. Maybe it's raising prices, cutting an underperforming expense, or doubling down on marketing that's working.

Common Income Statement Mistakes to Avoid

Mixing Personal and Business Expenses Keep them separate! Personal expenses don't belong on your business income statement, and mixing them makes it impossible to understand your true profitability.

Ignoring Small Expenses Those $10 monthly subscriptions add up. Track everything, even if it seems insignificant.

Not Categorizing Expenses Correctly Consistent categorization helps you spot trends. Don't put website hosting under "office supplies" one month and "marketing" the next.

Forgetting to Record All Income Every payment you receive needs to be recorded, even that small cash payment or Venmo from a friend-turned-client.

The Bottom Line

Your income statement isn't just a tax requirement—it's a powerful management tool that tells you whether your business model is working. By understanding this simple report and reviewing it monthly, you're taking control of your financial future.

You don't need an accounting degree to read an income statement. You just need to understand the basics we've covered here and commit to looking at your numbers regularly.

Remember: every successful business owner I know makes decisions based on data, not gut feelings. Your income statement provides that data.

Ready to get clarity on your numbers? If pulling together an accurate income statement feels overwhelming, or if you're not sure your books are set up correctly, I'd love to help. Proper bookkeeping gives you confidence in your numbers and peace of mind that you're making the right decisions. Book a free 30-minute consultation to discuss how I can support your business.