Quarterly Estimated Taxes Guide for Small Business Owners

Learn who pays estimated taxes, how to calculate them, IRS deadlines, and payment tools. Simple guide for freelancers, sole proprietors & startups.

TAX INFORMATION

Jerry Blanco

12/5/20257 min read

Never Get Caught Off-Guard by the IRS Again—Master Estimated Tax Payments in 15 Minutes

You've built something amazing. Whether you're a freelance graphic designer working from your kitchen table, a consultant with a growing team of three, or a startup founder juggling seventeen hats at once, you're making it happen. But then April rolls around, and your accountant drops a bomb: "You owe $8,000 in taxes—plus penalties for not paying quarterly."

Wait, what? Quarterly?

If you've ever felt that stomach-drop moment, you're not alone. Estimated taxes are one of those things nobody tells you about when you start a business. Unlike the W-2 job where taxes magically disappear from your paycheck, business owners have to proactively send money to the IRS four times a year. Miss those deadlines, and you'll face penalties that feel like adding insult to injury.

The good news? Once you understand the system, estimated taxes become just another routine part of running your business—like paying your phone bill, only with slightly higher stakes. Let's break this down into bite-sized pieces you can actually use.

Who Actually Needs to Pay Estimated Taxes?

Here's the simple rule: If you expect to owe $1,000 or more in taxes when you file your return, the IRS wants you to pay throughout the year, not all at once in April.

This typically includes:

Sole proprietors and freelancers: If you're a 1099 contractor, consultant, or running a side business, no employer is withholding taxes for you. That means you're responsible for both income tax and self-employment tax (which covers Social Security and Medicare—about 15.3% right off the top).

Partnerships: If you're splitting profits with business partners, each partner pays estimated taxes on their share of the income. The partnership itself doesn't pay income tax, but you do.

S-Corporation owners: Even if you pay yourself a W-2 salary, any additional distributions or profits might require estimated payments.

Anyone with significant side income: Rental properties, investment income, or that Etsy shop that suddenly took off—if it's not being withheld from a paycheck, you likely need to pay estimated taxes.

Think of it this way: the IRS operates on a "pay-as-you-go" system. They want their cut as you earn money, not months later. When you had a traditional job, your employer sent that money in every pay period. Now that's your job.

How Much Should You Pay? (The Math Made Simple)

I know, I know—math isn't why you started your business. But stick with me here. There are two main approaches to figuring out your estimated tax payments:

Method 1: Base It on Last Year (The Safe Harbor Rule)

This is the easiest route if your income is relatively stable. Pay 100% of what you owed last year (or 110% if your adjusted gross income was over $150,000), divided into four equal payments. Even if you earn more this year, you won't face penalties because you met the safe harbor threshold.

Example: Last year you owed $12,000 in total taxes. Divide that by four, and you'll pay $3,000 per quarter. Simple, predictable, done.

Method 2: Estimate This Year's Income

If your income fluctuates wildly or you're in your first year of business, you'll need to project your annual income and calculate taxes on that amount. Here's the simplified formula:

Estimate your total business profit (revenue minus expenses)

Multiply by your tax rate (federal income tax + 15.3% self-employment tax)

Divide by four for your quarterly payment

Example: You expect to make $80,000 profit this year. After deductions, you're in the 22% federal tax bracket, plus 15.3% for self-employment tax = roughly 37.3% total. That's about $29,840 in annual taxes, or $7,460 per quarter.

Feel overwhelmed? The IRS provides Form 1040-ES with a worksheet that walks you through this calculation step-by-step. Or better yet, use tax software or work with a bookkeeper who can run these numbers.

Pro Tip: It's smarter to slightly overestimate and get a refund than to underestimate and owe penalties. The IRS doesn't pay you interest on overpayments, but they definitely charge you interest on underpayments.

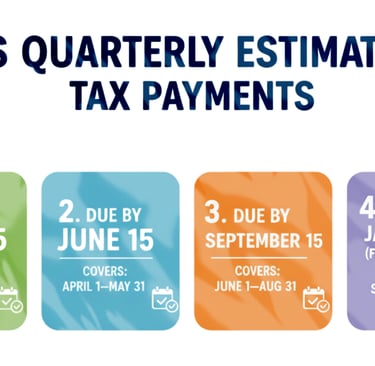

Mark Your Calendar: IRS Payment Deadlines

The IRS divides the year into four payment periods—but they're not exactly quarters in the calendar sense. Here are the deadlines (for most taxpayers):

April 15: Payment for January 1–March 31

June 15: Payment for April 1–May 31

September 15: Payment for June 1–August 31

January 15 (of the following year): Payment for September 1–December 31

Notice anything weird? That second "quarter" is only two months, while the third is three months. Please ensure these dates are recorded in all applicable calendars.

If a deadline falls on a weekend or holiday, it shifts to the next business day. And if you file your annual tax return by January 31 and pay your full balance due, you can skip that January 15 estimated payment entirely.

Set up reminders now. Put recurring alerts in your phone for two weeks before each deadline. Missing a payment triggers penalties that start at 0.5% per month—it adds up fast.

Tools & Methods: How to Actually Make These Payments

Gone are the days of writing checks and mailing them to some mysterious IRS address. You have options that make this process nearly painless:

IRS Direct Pay (Free)

Go to irs.gov/payments and pay directly from your checking or savings account. No fees, no registration required. You'll need your Social Security number and the amount you're paying. The system generates a confirmation number—screenshot it or write it down.

Electronic Federal Tax Payment System (EFTPS)

This free system (eftps.gov) requires enrollment, but once you're set up, you can schedule payments in advance. Schedule all four quarterly payments in January, and you'll never miss a deadline. You can also track your payment history, which is handy at tax time.

Credit or Debit Card

The IRS partners with payment processors that accept cards, but they charge convenience fees (usually 1.87–1.99%). Only worth it if you're earning credit card rewards that offset the fee—or if you're in a cash flow crunch and need the extra 30 days.

Pay Through Your Tax Software

QuickBooks Self-Employed, TurboTax, and similar platforms can calculate and submit estimated payments for you. They'll remind you when payments are due and keep records organized. Plans typically cost $10–30 per month, but the time savings and peace of mind often justify the expense.

Old-School Check

You can still mail Form 1040-ES with a check to the IRS. Just send it certified mail so you have proof of the postmark date. This method takes longer to process, and there's always a chance it gets lost in the mail—but it works if you're uncomfortable with digital payments.

My recommendation for most small business owners: Set up EFTPS and schedule your payments at the beginning of the year. Automate what you can, and free up mental bandwidth for actually running your business.

Smart Strategies to Make Estimated Taxes Less Painful

Open a Separate Tax Savings Account

This is hands-down the best advice I give new business owners. Open a separate savings account labeled "Taxes" and automatically transfer a percentage of every deposit you receive. Aim for 25–30% if you're just starting out. When quarterly deadlines arrive, the money is sitting there waiting—no scrambling, no stress.

Adjust as You Go

Your income won't be perfectly smooth throughout the year. If you have a killer second quarter, bump up your June payment. If things slow down in fall, you can reduce your September payment (just make sure you're still meeting safe harbor requirements to avoid penalties).

Deduct Your Estimated Tax Payments

While you can't deduct federal income tax itself, you can deduct the self-employment tax portion and any state/local estimated payments on your Schedule C or as an adjustment to income. Work with a tax professional to make sure you're capturing this benefit.

Consider Quarterly "Tax Meetings" with Yourself

Block 30 minutes before each deadline to review your income and expenses year-to-date. Adjust your estimated payment if needed. This quarterly check-in becomes a mini financial health assessment for your business—incredibly valuable beyond just taxes.

What Happens If You Don't Pay?

Let's talk about the scary part for a second—not to panic you, but to motivate you.

Underpayment penalties: If you owe $1,000+ and didn't pay enough throughout the year, the IRS charges interest on the underpaid amount. The rate changes quarterly (it's around 8% as of 2024) and compounds. On a $5,000 underpayment, you could easily owe an extra $400+ in penalties.

Estimated tax penalties are separate from late filing penalties. You can file your return on time and still get hit with underpayment penalties if you didn't pay enough quarterly.

The good news? If you meet safe harbor requirements (paying 100%/110% of last year's tax or 90% of current year's tax), you avoid penalties even if you owe a balance in April.

Your 3-Step Action Plan (Do This Today)

You've made it through the explanations—now here's exactly what to do next:

Step 1: Pull out last year's tax return (Form 1040). Look at line 24 to see your total tax. Divide that by four. That's your baseline quarterly payment using the safe harbor method. Write that number down.

Step 2: Go to eftps.gov or irs.gov/payments right now and make your next estimated payment if one is due soon. Set up an account so you're ready for next time. Don't put this off—deadlines sneak up faster than you think.

Step 3: Open that separate savings account for taxes this week. Set up an automatic transfer of 25–30% of your income into that account. Treat it like a bill you owe yourself. When tax time comes, you'll thank yourself profusely.

You've Got This

Estimated taxes feel like one more complicated thing on your already-full plate. But here's the truth: once you set up a system—even a simple one—it becomes routine. You're not just avoiding penalties; you're taking control of your business finances in a way that reduces stress and helps you sleep better at night.

And remember, you don't have to figure this out alone. That's why people like me exist. Whether you need someone to calculate those estimated payments, set up your bookkeeping system, or just answer questions when tax season rolls around, professional help is an investment in your peace of mind and your business's financial health.

What's your biggest estimated tax question or concern?

Ready to Stop Stressing About Taxes?