Payroll Basics for Small Business Owners | Simple Guide

Learn payroll fundamentals every small business owner needs to know. Understand taxes, deductions, cash flow impact, and compliance without the overwhelm.

PAYROLL

Jerry Blanco

10/24/20255 min read

The Essential Guide to Running Payroll Without the Headaches (Even If Numbers Aren't Your Thing)

You've done it—you've hired your first employee (or maybe your fifth). Congratulations! But then reality hits: Wait, how do I actually pay them?

If the word "payroll" makes your stomach flip, you're not alone. Most small business owners I talk to would rather focus on serving customers, creating products, or literally anything else. But here's the truth: getting payroll right isn't just about cutting checks. It affects your cash flow, keeps you out of trouble with the IRS, and—most importantly—shows your team you're a professional operation they can trust.

The good news? Payroll doesn't have to be mysterious or overwhelming. Let's break it down into bite-sized pieces you can actually use.

What Exactly Is Payroll (And Why Does It Matter So Much)?

Think of payroll as the entire process of compensating your employees—not just handing them money, but also handling all the taxes, paperwork, and reporting that comes with it.

Here's why it matters more than you might think:

Cash Flow Reality Check: Payroll is typically your biggest recurring expense. If you're not planning for it properly, you might find yourself scrambling when payday arrives. Unlike most business expenses, you can't just "skip" payroll or pay it late without serious consequences.

Legal Compliance: The government takes payroll taxes very seriously. Miss a deadline or miscalculate a tax, and you're looking at penalties that can seriously hurt a small business. I've seen entrepreneurs face fines that exceed their actual tax bill simply because they didn't know what they didn't know.

Employee Trust: Your team is counting on you. When paychecks are accurate and on time, you build loyalty and confidence. When there are constant mistakes or delays, even your best employees start updating their resumes.

The Building Blocks: Key Payroll Components You Need to Understand

Let's walk through the essential pieces of every paycheck. I promise this is simpler than it sounds.

Gross Pay: The Starting Point

This is what you agree to pay someone before anything gets taken out. If you hired someone at $20 per hour and they worked 40 hours, their gross pay is $800. For salaried employees, you divide their annual salary by your number of pay periods (usually 24 or 26 for bi-weekly pay).

Pro tip: Track hours carefully from day one. Use a simple time-tracking app, spreadsheet, or even a paper timesheet. You'll need this for hourly workers, and it's helpful for understanding where everyone's time actually goes.

Employee Deductions: What Comes Out of the Check

This is where it gets interesting. Before your employee receives their money, several things get deducted:

Federal Income Tax: This is withheld based on the Form W-4 your employees filled out when they started. The form considers their filing status, dependents, and other factors. Think of yourself as the middleman—you're holding this money and sending it to the IRS on your employee's behalf.

FICA Taxes: This covers Social Security (6.2% of gross pay) and Medicare (1.45% of gross pay). Your employee pays these percentages, but here's the kicker—you as the employer match these amounts dollar for dollar.

State and Local Taxes: Depending on where you're located, you might also withhold state income tax, local city taxes, or other regional requirements. Some states (like Texas, Florida, and Washington) don't have state income tax, which simplifies things slightly.

Other Deductions: This could include health insurance premiums, retirement plan contributions, or wage garnishments (if applicable).

After all these deductions, what's left is the net pay—the actual amount that hits your employee's bank account or appears on their physical check.

Employer Taxes: Your Share of the Bill

Here's what surprises most first-time employers: you owe taxes on top of what you pay your employees.

Employer FICA Match: Remember those Social Security and Medicare taxes your employee pays? You match them exactly—another 7.65% of their gross pay coming out of your business account.

Federal Unemployment Tax (FUTA): You pay 6% on the first $7,000 of each employee's wages per year. However, most businesses get a credit that reduces this to 0.6%, or $42 per employee annually.

State Unemployment Tax (SUTA): This varies wildly by state and by your company's claims history. New businesses typically start with their state's standard rate, which might be anywhere from 1% to 5% or more.

Real-world example: If you pay an employee $3,000 gross for the month, you're also paying roughly $230 in employer taxes on top of that. Many new business owners forget to budget for this additional 7-8% expense.

How Payroll Impacts Your Business Operations

The number one mistake I see? Business owners treating payroll like any other bill that can wait if cash is tight. You need to budget not just for the employee's check, but for:

Your employer tax portion (add roughly 8% to every dollar of wages)

The employee's withheld taxes (you're holding this temporarily, but it's not your money)

Any benefits you're covering

Actionable step: Create a separate bank account just for payroll. Every time money comes into your business, immediately transfer your estimated payroll costs (including taxes) into this account. When payday arrives, you'll have the funds ready and won't be tempted to "borrow" from payroll for other expenses.

Compliance and Record-Keeping

The IRS requires you to deposit withheld taxes on a specific schedule—either monthly or semi-weekly, depending on your total tax liability. Miss a deposit, and penalties start immediately.

You also need to file quarterly Form 941 reports and annual Form 940 for unemployment taxes. Each employee needs a W-2 by January 31st of the following year.

What to keep: Hold onto time sheets, pay stubs, tax deposits, and payroll registers for at least four years. If you're ever audited, this documentation is your defense.

Employee Satisfaction

Mistakes happen, but frequent payroll errors send a terrible message. Employees need to:

Receive consistent, predictable pay dates

Get accurate amounts without having to chase corrections

Access clear pay stubs that show what was deducted and why

Trust that their retirement contributions or insurance premiums are actually being sent where they should go

Your Next Steps: Getting Payroll Right From the Start

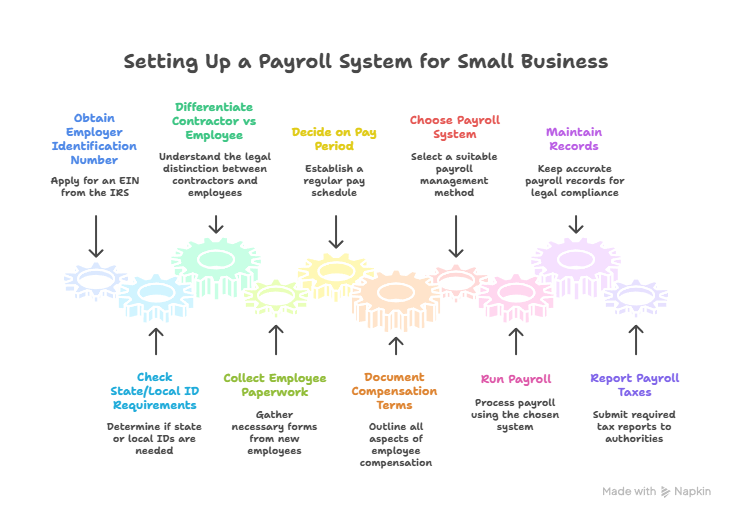

Step 1: Decide whether to handle payroll yourself or use a service. For most small businesses, payroll software (like Gusto, QuickBooks Payroll, or ADP) costs $40-150/month and handles calculations, tax deposits, and filing automatically. This is almost always worth the investment—your time is valuable, and one missed tax deposit can cost more than a year of service fees.

Step 2: Get your federal Employer Identification Number (EIN) if you don't have one already. You'll need this to report and pay payroll taxes. Apply for free at IRS.gov—it takes about 15 minutes.

Step 3: Register with your state agencies for unemployment insurance and state withholding (if applicable). Each state has different requirements and websites, but your state's Department of Revenue and Department of Labor are your starting points.

Step 4: Have every new employee complete a W-4 (federal), state withholding form (if applicable), and I-9 (employment eligibility verification). Keep copies of everything.

Step 5: Establish a consistent pay schedule and stick to it religiously. Most small businesses choose bi-weekly or semi-monthly schedules. Whatever you choose, put it in writing and communicate it clearly.

The Bottom Line

Payroll might feel intimidating right now, but it's really just a system—one that thousands of small business owners successfully manage every single day. The key is understanding the fundamentals, staying organized, and knowing when to ask for help.

You don't have to become a payroll expert. You just need to know enough to make smart decisions and recognize when something doesn't look right. That's exactly where a good bookkeeper or accountant becomes worth their weight in gold—they can set up systems that run smoothly so you can focus on growing your business instead of worrying about whether you calculated Social Security correctly.

Remember: every successful business owner you admire had to figure this out too. You've got this.